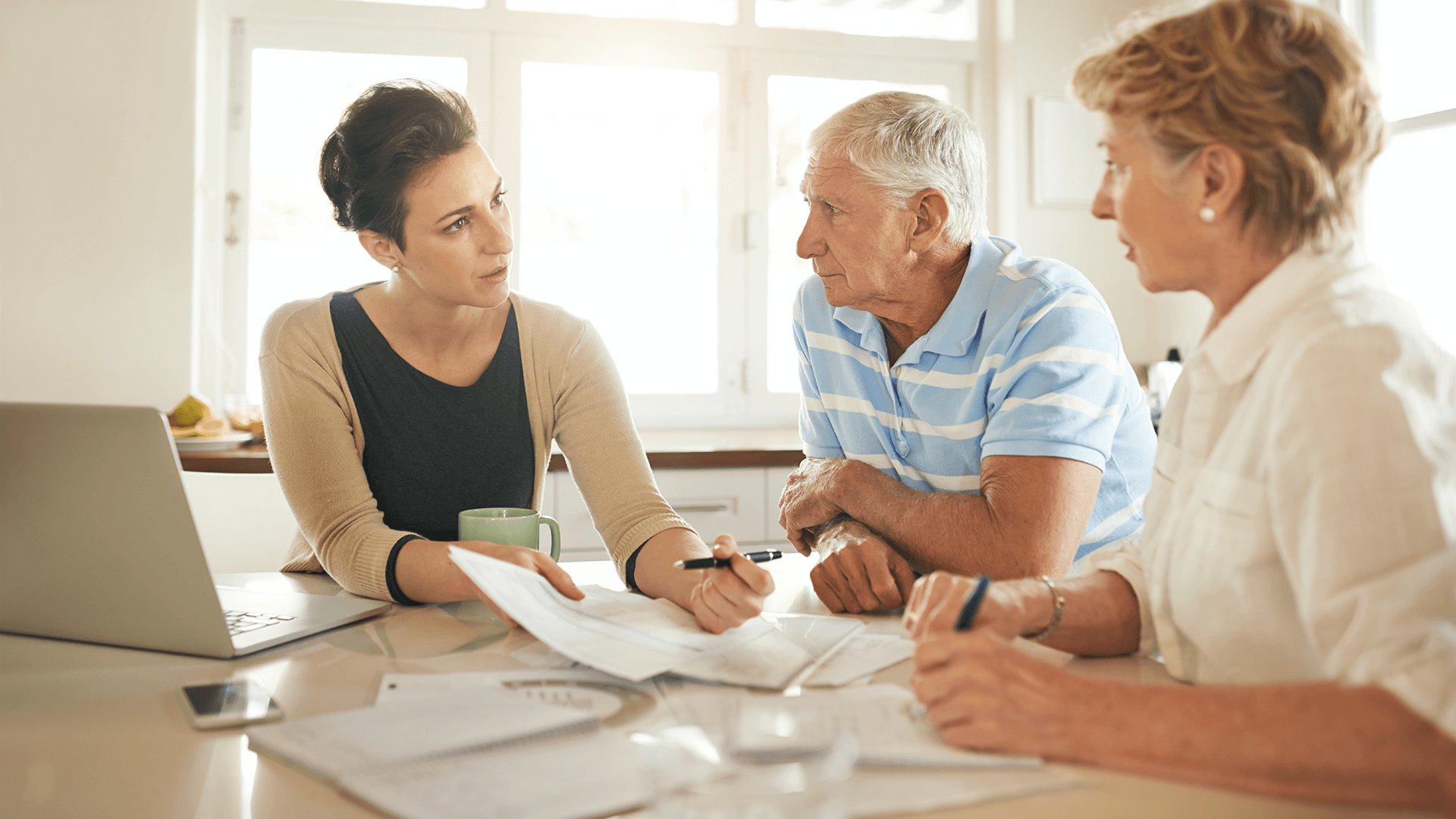

Many of us “boomers” are finding ourselves in the “sandwich generation.” It is a challenging situation where we take care of our parents while still supporting our adult children and perhaps strapped with their student loans.

While our young adult children struggle to achieve financial independence, the burden may fall on you. You are not alone. Nearly half of adults in their 40s and 50s have a parent age 65 or older and are raising a young child or financially supporting a grown child (age 18 or older). And less than 20% of middle-aged adults provide financial support to both an aging parent and a child.

According to a new nationwide Pew Research Center survey, 48% of adults ages 40 to 59 have provided some financial support to at least one grown child in the past year, with 27% providing the primary backing. Among adults who are 18 years and older who have a parent age 65 or older, just 32% provided financial help to a parent in the Pew research gourp1.

More affluent adults, those with annual household incomes of $100,000 or more, are more likely than less affluent adults to be in the sandwich generation. Among those with incomes of $100,000 or more, 43% have a living parent age 65 or older and a dependent child.

Financial support for aging parents and grown children

Many adults believe there is a responsibility to provide for an elderly parent in financial need; nearly a quarter of us do so. The financial assistance we provide to our aging parents is typically for ongoing expenses. This is very similar to the need to care for grown children. Overall, we are more likely to be providing financial support to a grown child than they are to an aging parent. Over half of American adults offer financial assistance to their grown children. The primary reason for doing so is because the child is enrolled in school. The financial burden falls heavily on baby boomers.4

Dealing with mortgage debt

According to the Joint Center, only about 20% of U.S. homeowners 65 and over had mortgage debt three decades ago. Economists calculate that about 40% of older Americans today have housing debt, and the median amount they owe has quadrupled after adjusting for inflation.

Boomers, unlike their parents, didn’t grow up in the Great Depression or celebrate paying off a mortgage with a note-burning party. They are more comfortable with debt as a strategic financial tool and don’t view tapping their homes for cash as the last resort that their parents did.

Fortunately for homeowners 60* years old or older, a reverse mortgage may be the optimum solution to minimizing or eliminating the generational sandwiches’ financial squeeze. When used properly, a reverse mortgage gives the options of receiving immediate tax-free cash, a monthly check for life, and a line of credit to be used if ever needed. Each of these options provides that no monthly mortgage payment is required, thereby increasing monthly cash flow. Of course, real estate taxes and insurance must be paid and abide by other loan guidelines.

Learn more about your options

Just like your 401K, IRA, or annuities, home equity is a powerful financial tool that can significantly enhance your retirement funding plan. Contact a Finance of

America Reverse, LLC (FAR) representative today to learn more about reverse mortgage benefits and how they may help you secure long-term financial freedom.

This article is intended for general informational and educational purposes only, and should not be construed as financial or tax advice. For more information about whether a reverse mortgage may be right for you, you should consult an independent financial advisor. For tax advice, please consult a tax professional.

I WANT TO KEEP UP TO DATE ON RETIREMENT TRENDS

Follow Us.